Migration

Shackles & Shambles: Capita and the electronic tagging boom

[Warning: mentions of suicide in the ‘benefits’ section] We are in the midst of a dramatic expansion of electronic tagging in the UK, but this is not without a strong pushback. Campaigners from Bail for Immigration Detainees, Migrants Organise,...

Latest Publications

Latest

Refurbish don’t demolish: the fight for the future of Thamesmead

Residents of Thamesmead, one of London’s largest and most iconic housing

Palantir in the UK: From the Ministry of Defence to the NHS

Palantir in the UK This is the second of two articles

Palantir: International Tech Despot

This is the first in two articles investigating US tech company,

Shackles & Shambles: Capita and the electronic tagging boom

[Warning: mentions of suicide in the ‘benefits’ section] We are in

The National Wealth Service: Players and Scandals

This is the second in a series of three articles investigating

The National Wealth Service: NHS Privatisation Timeline

This is the third in a series of three articles investigating

The National Wealth Service: Privatisation Profiteers

This is the first in a series of three articles investigating

Who’s arming Israel? Mapping UK sites linked to Israeli state terror

This is the first part of a project naming and locating

It’s time to Make Amazon Pay: how you can take action on Black Friday

Amazon is one of the world’s largest companies and a high-tech

Beyond Divestment: BP & Shell show fossil fuel divestment campaigns aren’t working

In our second investigation into BP and Shell’s shareholders in collaboration

The Cost of Misery: Rising Millions in the Bibby Stockholm Fiasco

A Home Office response to Freedom of Information requests submitted by

Bristol City Council & Goram Homes forcing Traveller evictions

Bristol City Council is planning to imminently force members of the

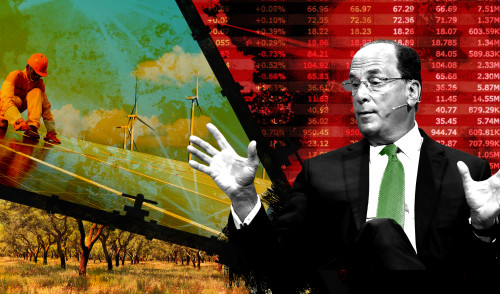

Carbon Cash Machine: What if BP & Shell dividends were used for the common good?

As part of our investigation with Queen Mary University’s Centre for Climate Crime and

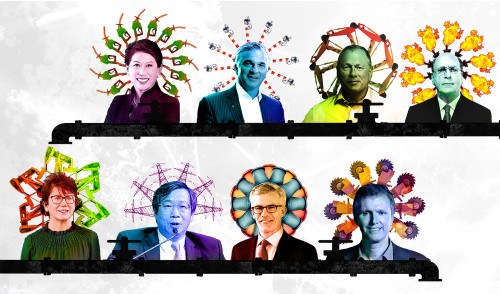

Carbon Cash Machine: meet the investors running – and destroying – our world

As part of our investigation with Queen Mary University’s Centre for

Carbon Cash Machine: charting the payouts to BP and Shell shareholders

In collaboration with Queen Mary University’s Centre for Climate Crime and